A financial institution's physical location facilitates direct deposit transactions. This location, often a bank branch, allows individuals to establish accounts and receive funds electronically. For instance, payroll checks or government benefits can be deposited directly into a designated account at a specific branch. The physical presence of a branch is sometimes necessary for account opening procedures or to reconcile account balances in person, though many of these activities are now available online or by phone.

This service, regardless of the specific location, offers numerous advantages. It eliminates the need for paper checks, saving resources and reducing risks of loss or theft. Furthermore, direct deposit ensures funds are available immediately into the recipient's account and typically avoids delays associated with check processing. This speed is crucial for timely access to funds, especially when dealing with essential payments. The security of electronic funds transfer is generally considered higher than traditional mail delivery of checks. Efficient and secure delivery of funds is significantly improved by the established infrastructure connecting the branch to the financial network.

This fundamental aspect of banking is crucial to understanding the wider topic of financial transactions. The next sections will explore the specifics of account opening procedures, account maintenance, and security measures associated with direct deposits. They will also examine the evolving role of bank branches in the digital age of banking.

Bank Branch Meaning for Direct Deposit

Direct deposit, a vital banking service, relies on bank branches for various crucial functions. Understanding these functions is essential for navigating the financial system effectively.

- Physical Location

- Account Setup

- Funds Transfer

- Account Access

- Transaction Verification

- Support Service

Bank branches are physical locations where direct deposit accounts are opened and maintained. This physical presence provides a point of contact for account setup, allowing for in-person verification and interaction. The branch's role in transferring funds through the banking network is critical. Branches facilitate account access for verifying transactions and resolving issues. Lastly, branch staff provide support, answering questions and addressing concerns, thus, enhancing the user experience. For example, an employee's paycheck might be directly deposited into their account at a particular branch, which validates the transaction and provides account access. These multifaceted functions underscore the enduring importance of bank branches in the direct deposit system.

1. Physical Location

The physical location of a bank branch is intrinsically linked to the meaning of direct deposit. A branch serves as a tangible point of contact for establishing and managing accounts essential for direct deposit operations. This physical presence enables crucial steps, including initial account setup, identity verification, and in-person assistance. Without a physical location, the process of opening an account for direct deposit would be significantly more complex and potentially less secure, relying solely on remote interactions.

Consider a scenario where an individual needs to open a direct deposit account for receiving government benefits. The physical branch provides a secure environment for verifying identity, completing necessary paperwork, and setting up the direct deposit mechanism. This in-person interaction enhances security, ensuring the account is established for the intended recipient and not subject to fraudulent activity. Similarly, a physical branch serves as a point of contact for resolving discrepancies in a direct deposit transaction, providing an opportunity for direct communication and resolution. These scenarios highlight the practical value of a physical branch in the direct deposit process.

In conclusion, the physical location of a bank branch is fundamental to the operational integrity and security of direct deposit. Its role extends beyond mere accessibility; it facilitates crucial interactions, verifies identities, and enables tailored support in managing direct deposit accounts. While the digital age is transforming banking, the enduring importance of a physical branch remains significant, especially when security and in-person assistance are required.

2. Account Setup

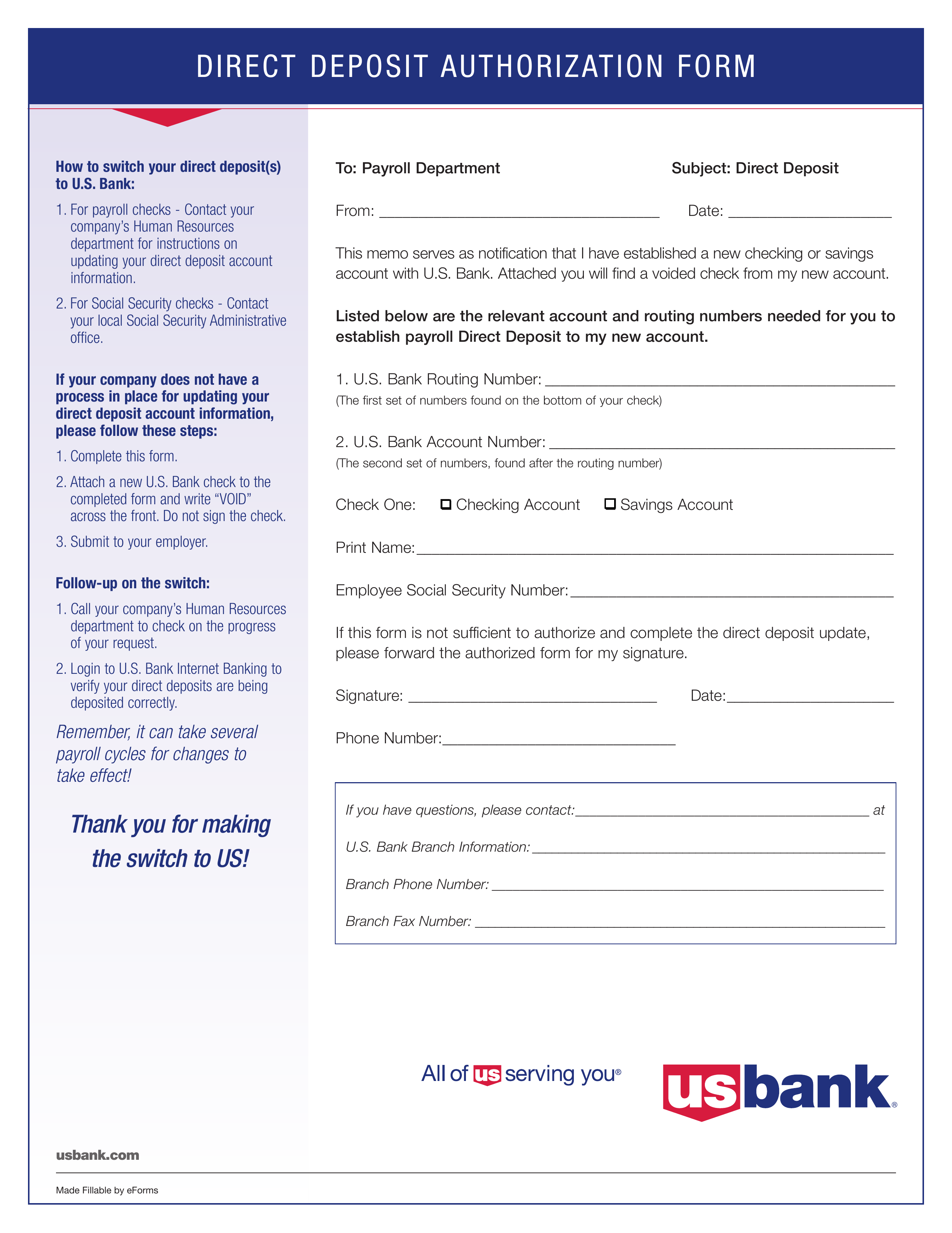

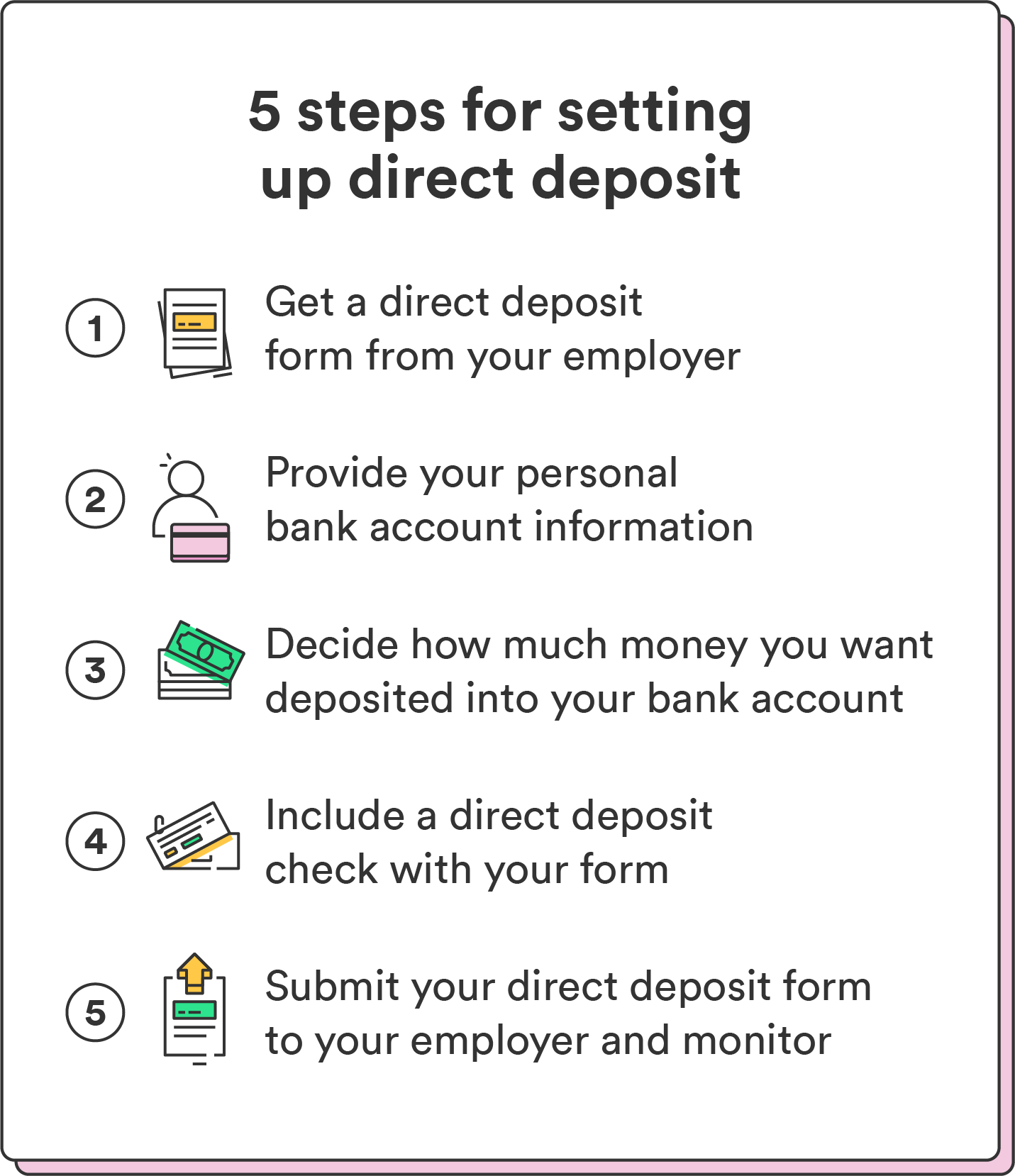

Account setup is a critical component of the direct deposit process, and bank branches play a crucial role in this stage. The physical presence of a branch facilitates account creation, ensuring secure and compliant procedures. Account opening necessitates in-person verification to mitigate risk of fraud, a critical function fulfilled at a branch. This verification often includes identity proofing, ensuring the account is established for the legitimate account holder. In-person setup also allows for thorough explanation of direct deposit procedures, ensuring the account holder understands how to use the service and the responsibilities associated with it. This is particularly important for individuals unfamiliar with electronic banking.

A real-world example illustrates this connection. Imagine an individual seeking to receive government benefits through direct deposit. The physical branch offers a secure environment to open the account, verify identity documents, and explain the direct deposit process. Without the branch, this process would be significantly more challenging, potentially involving complex online procedures that lack the immediacy of in-person verification. This security aspect is particularly critical in preventing fraudulent account setups. The branch provides immediate assistance in addressing any questions or concerns during the account setup process, thus ensuring a smooth and secure transition to direct deposit.

A thorough understanding of account setup within the context of a bank branch is essential. This understanding acknowledges the crucial role of the branch in the direct deposit system, highlighting security and support in account establishment. This is important for individuals seeking to use this banking service, and institutions ensuring secure and correct processing of transactions. This aspect emphasizes the ongoing value of a physical branch despite the growth of digital banking.

3. Funds Transfer

Funds transfer, a core function of direct deposit, is intricately linked to the operational meaning of a bank branch. Branches act as intermediaries in the electronic transfer of funds. Direct deposit relies on a bank's infrastructure and personnel to process these transactions. This includes verifying account details, ensuring sufficient funds are available, and routing the funds to the designated recipient's account. Without the physical or virtual infrastructure of the branch, direct deposit transactions cannot occur reliably or securely.

Consider a payroll transaction. Employee paychecks are deposited directly into designated accounts. The bank branch, either physically or digitally, verifies the payroll information, confirms funds availability in the employer's account, and initiates the transfer to the employee's account. This process typically involves numerous steps, including data validation, security protocols, and confirmation messages. The branch facilitates this entire sequence from beginning to end. Similarly, government benefits disbursement relies on similar processes, ensuring timely and accurate transfer of funds to eligible recipients.

The importance of this understanding cannot be overstated. A well-functioning funds transfer system, facilitated by the presence of a bank branch, ensures timely access to funds, reduces the risk of errors, and enhances overall financial security. Without a strong understanding of how branches facilitate these transfers, users might struggle to understand the operational complexities behind direct deposit or experience delays, errors, or fraudulent activity. Moreover, the efficiency of these transfers is essential to the operation of businesses, governments, and individual financial well-being.

4. Account Access

Account access, a critical aspect of direct deposit, is intrinsically linked to the operational significance of a bank branch. The ability to access an account, particularly for direct deposit transactions, depends on various procedures and systems that are often facilitated by the presence of a branch. This access encompasses not only viewing account balances but also initiating and monitoring transactions, a crucial function for users reliant on direct deposit services.

- In-Person Verification and Support

A physical branch offers a readily available point of contact for verifying account details, resolving discrepancies, and receiving immediate support. This personal interaction is crucial for resolving issues, such as verifying identity for access to funds or addressing questions about direct deposit transactions. The ability to interact face-to-face with branch personnel is a critical component of account access for many users, especially those unfamiliar with online banking or requiring personalized support.

- Transaction Monitoring and Reconciliation

Branches enable immediate reconciliation of transactions, particularly useful for direct deposit. Customers can quickly check the status of a direct deposit to ensure funds have been credited correctly, verifying the accuracy of the transaction. This in-person access allows for efficient problem resolution and prevents delays or potential fraud. The physical presence of a branch can be a critical factor in managing direct deposit transactions and maintaining account security.

- Account Maintenance Procedures

Establishing, modifying, or closing direct deposit accounts frequently necessitates in-person interaction at a branch. This includes updating contact details, adding or removing deposit instructions, or changing account access information. The branch serves as the point of contact for these essential procedures, ensuring that direct deposit functions correctly. These steps underscore the branch's ongoing importance in account maintenance and the security of direct deposit services.

- Limited Online Access Considerations

While online access to accounts is commonplace, certain direct deposit procedures or issues may require access to the branch to address. The ability to use the branch for in-person assistance or transaction verification is crucial when online tools and support are insufficient or unavailable for a specific issue. This highlights the continued need for branches in a digital banking environment.

In summary, account access, particularly in the context of direct deposit, is multi-faceted. The ability to readily access and manage accounts, including direct deposit transactions, is significantly enhanced by the presence of a bank branch. This includes in-person verification, transaction monitoring, account maintenance, and the provision of support when online access is insufficient or unavailable. The branch's role is integral to the smooth operation and security of direct deposit services, even in an increasingly digitized financial landscape.

5. Transaction Verification

Transaction verification is a critical component of direct deposit, and the presence of a bank branch plays a significant role in ensuring accuracy and security. Proper verification procedures, whether conducted in person or remotely, are paramount to maintaining the integrity of the entire process. This section examines the multifaceted nature of transaction verification within the context of bank branches and direct deposit.

- In-Person Verification

Bank branches offer a physical space for in-person verification, crucial in cases involving account ownership disputes or unusual transactions. This direct interaction enables immediate identification and authentication, resolving potential issues promptly. For instance, verifying a payee's identity during the initial account setup for direct deposit or addressing discrepancies in a deposit prevents fraudulent activity. The presence of a branch is especially vital for situations requiring immediate clarification.

- Document Validation

Branch staff can verify crucial documents, such as government-issued IDs, to ensure the accuracy and legitimacy of direct deposit transactions. This document validation is vital in preventing fraudulent activity and ensuring the funds are sent to the intended recipient. For example, a government agency might require documentation verification for direct deposit payments for social security benefits, mitigating the risk of misdirected funds.

- Discrepancy Resolution

A bank branch acts as a point of contact for resolving discrepancies related to direct deposit transactions. This might include correcting errors in account details, addressing insufficient funds issues, or resolving problems stemming from incomplete or incorrect information. This swift resolution, facilitated in-person, minimizes disruptions to the payee's funds.

- Transaction Monitoring and Reconciliation

Branch personnel can assist in monitoring and reconciling direct deposit transactions, ensuring accuracy and efficiency. Customers can seek verification of transaction details to confirm the expected amount and the time frame for the fund's arrival. This active monitoring, both in person or remotely by trained staff, is vital in identifying and addressing anomalies.

In conclusion, transaction verification is not a singular action but a multifaceted process where the bank branch plays a pivotal role. From initial account set-up to resolving discrepancies, the presence of a branch enables secure and accurate direct deposit transactions. This in-person verification process, coupled with the ability to validate documents, resolve issues, and monitor transactions, is essential for the integrity and security of direct deposit. Even with the increasing use of digital tools, the role of the branch in ensuring secure transaction verification remains essential.

6. Support Service

Support services offered at bank branches are inextricably linked to the meaning of direct deposit. A robust support system is essential for the smooth functioning and security of direct deposit transactions. This support encompasses a range of services, from assisting with account setup and troubleshooting technical issues to resolving disputes and answering questions regarding the direct deposit process. Effectively addressing customer inquiries is crucial to building trust and maintaining a positive user experience, a factor that directly impacts the reliability of the direct deposit system. The immediate availability of human assistance offered by a branch is critical in situations involving errors, delays, or security concerns. Without adequate support, the efficacy and security of direct deposit become vulnerable.

Real-world examples underscore the importance of support services at branches. Imagine a situation where a customer experiences a delay in a direct deposit for their paycheck. The immediate access to branch staff allows for quick verification and resolution of the issue, minimizing financial distress. Alternatively, a customer may have questions about updating direct deposit instructions or experience difficulties in navigating the online portal. Branch personnel are equipped to guide customers through these procedures, ensuring a smooth and secure transaction. These scenarios demonstrate the practical significance of support services in mitigating potential issues associated with direct deposit and maintain customer confidence.

In conclusion, the support services provided at bank branches are fundamental to the effective operation and security of direct deposit systems. These services not only help customers navigate the process but also play a crucial role in preventing errors, resolving disputes, and maintaining user confidence in the direct deposit system. A well-equipped support system is essential to building trust and ensures reliable access to financial resources. This connection highlights the continued importance of bank branches as points of support within a complex digital financial landscape.

Frequently Asked Questions

This section addresses common inquiries regarding the role of bank branches in the direct deposit process. Understanding these details is crucial for navigating the financial system effectively.

Question 1: What is the role of a bank branch in facilitating direct deposit?

Bank branches act as intermediaries in the direct deposit process. They provide a physical location for account setup, verification, and ongoing support. This includes crucial functions like verifying identities, validating account information, and resolving any discrepancies that may arise during or after a direct deposit transaction. Branch staff play a critical role in guiding customers through the process, especially those unfamiliar with electronic banking procedures.

Question 2: Is a bank branch still necessary for direct deposit in the digital age?

While online banking is prevalent, bank branches remain essential for direct deposit. Physical branches provide critical in-person verification and support that online systems may not readily offer. In situations requiring identity confirmation, document validation, or complex issue resolution, a branch's support is invaluable. Furthermore, some individuals may prefer in-person interaction for account setup or maintenance.

Question 3: How does a bank branch ensure the security of direct deposit transactions?

Bank branches employ robust security measures to safeguard direct deposit transactions. These include rigorous identity verification procedures, secured environments for document handling, and trained staff to address security concerns. They also adhere to industry best practices and regulations to minimize the risk of fraudulent activity. Furthermore, the physical presence of a branch enables immediate response to potential security breaches.

Question 4: Can I open a direct deposit account entirely online without visiting a branch?

While some banks offer online account opening, it may not be possible to complete the full direct deposit account setup entirely online. Many institutions require in-person verification for security reasons. This in-person visit enables the bank to properly validate the account holder's identity and confirm the account's intended use for direct deposit.

Question 5: What if I experience a problem with a direct deposit transaction?

If a problem arises with a direct deposit, a bank branch is a crucial resource for resolution. Branch staff are trained to address issues such as insufficient funds, incorrect account information, or delayed payments. They can provide assistance in reconciling the transaction, verifying details, and ensuring a swift resolution. Direct contact with the branch facilitates a more expedient approach compared to online support.

Question 6: How do government benefits relate to the bank branch's role in direct deposit?

Bank branches are critical for distributing government benefits via direct deposit. They provide the physical locations for establishing accounts and receiving funds. Often, government agencies require in-person interaction at a branch for account setup and verification to prevent fraud, underscoring the crucial role of branches in this system.

In conclusion, bank branches play a multifaceted role in the direct deposit system. Their function extends beyond simply being a location; they are essential for ensuring security, resolving issues, and providing support to clients. This multifaceted role is crucial for the smooth and secure operation of the entire process.

The following sections will delve deeper into account setup procedures, security measures, and the evolution of direct deposit in the modern financial landscape.

Tips Regarding Bank Branch Role in Direct Deposit

Navigating the direct deposit process effectively requires understanding the crucial role bank branches play. These tips offer practical guidance for users and institutions alike.

Tip 1: Verification is Paramount. Accurate account information is fundamental to direct deposit. Thorough identity verification procedures at a branch minimize fraud risks and ensure funds reach the intended recipient. This may involve presenting government-issued identification and verifying account details against records. Failure to properly verify can lead to delays or financial losses.

Tip 2: Documentation is Essential. Maintaining accurate records of direct deposit information, including account numbers and routing information, is critical. This documentation facilitates smooth transaction processing and problem resolution. These records help both the sender and recipient track funds in transit.

Tip 3: Know the Process. Understanding the steps involved in a direct deposit transaction, from account opening to funds transfer, is vital. Familiarity with account maintenance procedures and the resolution of potential issues ensures a smooth experience.

Tip 4: Support Services are Available. Branch staff are trained to handle inquiries and resolve issues related to direct deposits. Utilizing these support services promptly can address problems quickly and effectively. This support extends to navigating online tools as well.

Tip 5: Regular Account Monitoring is Crucial. Checking account balances and transaction history routinely helps identify potential errors or discrepancies. Prompt identification of issues allows for timely resolution, reducing potential delays and safeguarding funds. This careful monitoring is vital in a system of electronic funds transfer.

Tip 6: Security Measures Should be Prioritized. Employing strong passwords and practicing caution when sharing financial information is crucial. Keeping sensitive information secure, whether online or in person, is paramount to preventing unauthorized access. Maintaining this level of security is a shared responsibility between institutions and customers.

Tip 7: Understand Legal Requirements. Depending on the jurisdiction or type of direct deposit, specific legal requirements may apply. Understanding and adhering to these regulations ensures compliance and minimizes legal complications. This often includes specific documentation requirements that customers should be aware of.

Adhering to these tips enhances the efficiency, security, and overall success of the direct deposit process. By understanding the various aspects of the bank branch's role, users can manage their funds effectively and mitigate potential risks. Awareness of these best practices contributes significantly to a user-friendly experience for all parties involved.

The subsequent sections will delve into the specifics of account setup, transaction security, and the evolution of direct deposit in the digital age.

Conclusion

This exploration of "bank branch meaning for direct deposit" reveals the multifaceted role these institutions play in the modern financial landscape. Bank branches are not simply physical locations; they are crucial intermediaries in the secure and efficient transfer of funds. Their function encompasses critical aspects like account opening, identity verification, transaction processing, and ongoing support, each essential for the reliability and security of direct deposit systems. The ability to establish and manage accounts in person, coupled with the availability of immediate support, enhances the legitimacy of transactions and mitigates potential risks associated with digital systems. Furthermore, branches facilitate reconciliation processes and address discrepancies, ensuring the accuracy and timely delivery of funds. This crucial role is particularly evident in processes involving government benefits and payroll disbursements.

The enduring importance of bank branches, despite the growth of digital banking, underlines the value of both physical and virtual interactions in financial transactions. The evolution of financial technology necessitates a nuanced understanding of how these elements seamlessly integrate to deliver efficient and secure direct deposit services. A complete appreciation of the complex interplay between technology and human interaction within the financial sector ensures the continued success and reliability of systems like direct deposit. This critical link between physical presence and electronic transfers forms the foundation for the ongoing evolution of secure and trusted financial practices.