This payment platform facilitates purchasing goods or services through a deferred payment system. Customers can acquire items now, and pay for them in installments over a set period. For example, a consumer might purchase a new television and receive a payment plan to cover the cost in manageable monthly amounts.

The platform's primary benefit lies in providing access to products and services that might otherwise be unaffordable upfront. This can stimulate consumer spending and potentially support economic activity. The flexibility of payment plans can be an attractive option, especially for larger purchases. However, interest or fees associated with installment plans need to be carefully considered. The service's impact on credit scores, and overall financial well-being of users, warrants careful consumer evaluation.

This discussion will further examine the implications of this payment method on retail businesses, consumer behavior, and financial markets. Subsequent sections will explore the various aspects of the platform in greater detail.

Sezzle Pay

Sezzle Pay, as a payment method, presents a complex interplay of financial and consumer factors. Understanding its key aspects is crucial for evaluating its impact.

- Installment payments

- Deferred purchases

- Flexible terms

- Interest rates

- Consumer access

- Retail partnerships

- Financial implications

- Credit score impact

The installment nature of Sezzle Pay offers immediate access to goods, but fluctuating interest rates and hidden fees can complicate long-term financial planning. Retailers benefit from increased sales, but consumer awareness about the costs of deferred payments is crucial. The service's effect on credit scores demonstrates a delicate balance between consumer convenience and financial responsibility. Understanding each of these elements is vital for a complete picture of Sezzle Pay's overall impact on the modern marketplace.

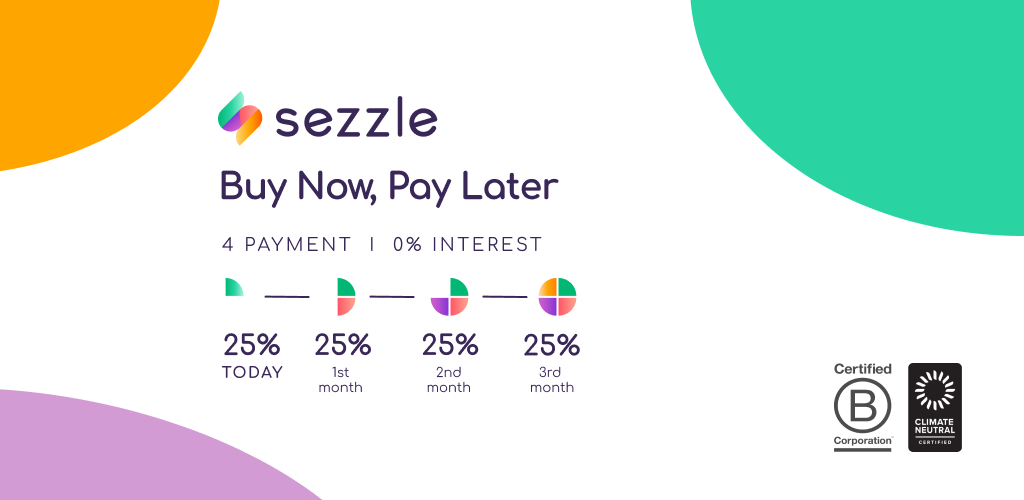

1. Installment Payments

Installment payments form the cornerstone of platforms like Sezzle Pay. This method allows consumers to acquire goods or services now, with the cost divided into smaller, predetermined payments over time. The core function of installment payments is to break down the total cost, making it potentially more accessible and manageable for consumers facing larger upfront expenses. Examples range from purchasing electronics to covering travel costs. The appeal lies in the immediate gratification of possessing the item coupled with the perceived reduced financial burden.

A crucial aspect of installment payments, within the context of Sezzle Pay, is the embedded financial terms. These include interest rates, fees, and the overall duration of the payment plan. Consumers need to carefully evaluate these terms, as failure to adhere to the agreed-upon payment schedule can lead to penalties, accruing additional costs. Careful financial planning and evaluation of affordability are essential components of responsible use. The understanding of installment payments, specifically within the framework of platforms like Sezzle Pay, is therefore crucial for informed consumer decisions. A detailed comprehension of potential interest rates and hidden fees is paramount to avoid unforeseen financial strain. This knowledge is vital to maximize the potential benefits of the service and mitigate the associated risks.

In conclusion, installment payments are integral to Sezzle Pay's operation. While providing immediate access to goods and services, consumers must thoroughly understand the associated financial implications. This includes calculating total costs, evaluating repayment schedules, and comprehending potential penalties. This knowledge allows consumers to make informed decisions and navigate the platform effectively, ensuring a positive financial experience.

2. Deferred Purchases

Deferred purchases are central to the functionality of platforms like Sezzle Pay. These systems allow immediate acquisition of goods or services, with the payment obligation spread across a set timeframe. The core concept is postponing full payment while still acquiring the product. This arrangement alters the traditional model of purchasing, where the transaction and payment occur concurrently. The ability to defer purchases acts as a significant component of Sezzle Pay's value proposition, appealing to consumers seeking flexibility and potentially encouraging spending in areas where upfront costs might be prohibitive.

Consider the example of a consumer wanting a new appliance. Without deferred purchase options, the consumer might need to save a substantial sum of money beforehand. With a deferred purchase platform, the consumer gains immediate access to the appliance, while the cost is broken down into manageable installments. This accessibility can influence purchase decisions, particularly when considering major purchases or items with a high upfront cost, such as furniture, electronics, or vacations. The practical significance of this understanding is substantial in both consumer economics and retail strategies. Consumers may consider more expensive items if they can be obtained now, whereas retailers gain increased sales volume by offering installment options. Consequently, deferring purchases shifts the focus from a purely immediate payment structure to a model that emphasizes access and affordability over immediate liquidity.

The concept of deferred purchases, exemplified by platforms like Sezzle Pay, alters the dynamics of consumer spending. By allowing immediate access to goods, it effectively broadens the range of purchases accessible to those with limited immediate financial resources. This convenience, however, comes with its complexities, including interest rates, fees, and potential for financial strain if not managed responsibly. A critical aspect for consumers and businesses to appreciate is the long-term financial implications of deferred purchases and how they impact budgeting and financial well-being.

3. Flexible Terms

Flexible terms, a defining characteristic of platforms like Sezzle Pay, represent the core of the deferred payment system. The ability to customize payment schedules and durations is key to attracting consumers and driving retail activity. Understanding the nuances of these terms is crucial for evaluating the potential benefits and risks involved.

- Payment Schedules

The variety of payment schedules offered, spanning from shorter-term, high-frequency payments to longer-term, lower-frequency options, directly addresses the diverse financial situations of consumers. This flexibility enables users to tailor their repayment strategy to fit their individual budgets. For instance, a user might choose a quicker repayment schedule for a smaller purchase, maximizing immediate access to the item while maintaining a strong cash flow. Conversely, for larger purchases, a longer repayment schedule might be preferred, ensuring a manageable monthly payment. Different schedules directly impact the overall cost of the purchase by influencing interest rates and potential fees.

- Duration Options

The range of payment durations offered by platforms like Sezzle Pay presents an array of choices. Options might span from several months to a year or more, depending on the purchase amount. This range caters to different spending patterns and financial capabilities. Longer durations might attract consumers needing greater payment flexibility, while shorter durations prioritize quick repayment and potentially offer a lower overall cost or risk. These varying options provide an essential level of customization within the installment payment system.

- Impact on Total Cost

The relationship between flexible terms and total cost is significant. While flexible schedules offer payment flexibility, they also impact the overall cost of the purchase. Longer payment durations frequently correlate with higher interest rates and potential fees, thereby increasing the total cost compared to shorter payment terms. Understanding this connection is critical to making informed decisions. Consumers should carefully analyze the total cost over the life of the loan, rather than solely focusing on the monthly payment amount.

- Consumer Choice & Financial Management

Flexible terms empower consumers with greater control over their spending habits. Consumers can align payment schedules with their current financial state and expected future cash flow. By selecting appropriate terms, individuals can manage their financial commitments effectively. However, this flexibility also demands careful planning and a realistic evaluation of one's financial capacity. This allows consumers to balance immediate needs with long-term financial well-being.

In conclusion, flexible terms are a critical component of platforms like Sezzle Pay, enabling consumers to tailor payment options to their unique financial circumstances. However, thorough understanding of the implications of different durations, schedules, and the impact on overall costs is paramount to making financially responsible decisions. Consumers must balance the convenience of flexible terms with the long-term financial ramifications to ensure a positive experience and avoid potential pitfalls.

4. Interest Rates

Interest rates are a critical component of deferred payment platforms like Sezzle Pay. They directly influence the overall cost of a purchase for the customer and significantly affect the profitability for the platform and participating merchants. Understanding how these rates function is essential for navigating the financial implications of such systems.

- Impact on Consumer Cost

Interest rates on installment plans directly translate into higher total purchase costs for consumers. A higher rate on a purchase paid in installments results in a greater overall expense than paying in full upfront. This additional cost is frequently expressed as a percentage of the total purchase price or as a specific fee over time. Variations in interest rates influence the final amount paid by the customer, shaping the perceived value of the purchase.

- Relationship with Payment Duration

The duration of payment plans significantly impacts interest rate structures. Longer payment periods often correlate with higher interest rates. This is because the lender or platform incurs risk over a more extended period, requiring a higher return on investment. Conversely, shorter payment plans generally accompany lower interest rates, reducing the overall financial burden for the customer. This correlation underscores the trade-off between convenience and cost for the consumer.

- Influence on Profitability

Interest rates are instrumental in determining the profitability of deferred payment platforms. Platforms generally aim to earn a return on the money extended to consumers. Higher interest rates increase the platform's revenue, but potentially increase the risk of customer dissatisfaction if rates are excessively high. Strategies for managing interest rates are vital for platform sustainability and long-term success.

- Comparison to Traditional Financing

Interest rates on platforms like Sezzle Pay should be compared with traditional financing options, such as credit cards or loans. Understanding the structure of interest rates allows consumers to make informed decisions. By comparing interest rates, fees, and potential costs, consumers can assess the overall financial implications of different payment options, choosing the one most aligned with their needs and circumstances.

In summary, interest rates are a fundamental aspect of deferred payment platforms. Their impact extends beyond simply influencing the total cost of a purchase; they also determine profitability for the platform and pose significant considerations for consumers. A comprehensive understanding of the relationship between interest rates, payment duration, and profitability allows a more informed evaluation of such payment systems. Consumers need to be aware of the total cost of borrowing money, whether via traditional or installment methods, and how the chosen approach aligns with their overall financial health.

5. Consumer Access

Consumer access is inextricably linked to platforms like Sezzle Pay. The system's design hinges on making goods and services accessible to a broader segment of consumers who might not possess the immediate financial resources to acquire them outright. This accessibility, in turn, influences retail strategies and consumer behavior.

The key mechanism is the deferred payment option. This allows consumers to purchase products or services now and pay for them in installments. This flexibility is particularly beneficial for individuals with limited immediate cash reserves but with the capacity to make regular, smaller payments. Real-world examples include purchasing a new appliance, covering travel costs, or upgrading technology without needing to save a substantial sum initially. This broadens access to a wider range of products and experiences previously out of reach for some consumers.

However, the concept of consumer access within Sezzle Pay is not without its caveats. The availability of deferred payment options could potentially lead to overspending if not managed responsibly. The ease of acquiring goods through installment plans may create a financial burden if not properly considered in the context of overall budget management. This critical point underscores the importance of consumer awareness and financial literacy in using services like Sezzle Pay effectively.

Furthermore, while consumer access is enhanced, the impact on consumer credit scores and long-term financial health needs careful consideration. A deeper understanding of the terms and conditions of installment payments, including interest rates, fees, and potential late payment penalties, is crucial. This awareness directly influences consumer behavior in leveraging this form of payment and highlights the importance of financial education and responsible use of these services.

In conclusion, consumer access is a defining feature of Sezzle Pay. The system aims to extend purchasing power to a wider customer base, influencing retail strategies and consumer decisions. However, consumers must understand the associated implications, including the potential for financial strain if not managed responsibly. Promoting financial literacy and responsible utilization of deferred payment options is essential for maximizing the positive impacts of these systems while mitigating potential risks for consumers.

6. Retail Partnerships

Retail partnerships are fundamental to the success of platforms like Sezzle Pay. These collaborations are vital for the platform's growth and the expanded reach of its services. Retailers gain access to a wider customer base and often, increased sales volume. Conversely, the platform benefits from a broader product selection, reaching diverse consumer demographics.

The nature of the partnership typically involves retailers integrating the platform's payment options into their existing systems. This allows consumers to choose Sezzle Pay as a payment method at the point of sale. Examples include online retailers allowing customers to select Sezzle as a payment option during checkout or brick-and-mortar stores displaying Sezzle signage and accepting the payment method. The implementation can vary greatly from a simple integration to more complex systems, reflecting the diverse needs of different retailers. The practical significance of these partnerships is in facilitating increased sales for businesses and providing more options for customers.

The success of the partnership hinges on mutual benefits. Retailers benefit from expanded sales and potentially reduced customer acquisition costs. Sezzle Pay, in turn, benefits from increased user engagement and a wider product selection. This dynamic drives broader market reach and potentially leads to higher overall adoption of the service. However, the ongoing challenges include ensuring seamless integration of the platform with existing systems, maintaining competitive interest rates, and ensuring customer satisfaction, which ultimately impacts the long-term success of both partners. A strategic understanding of these interconnected roles is crucial for sustainable growth.

7. Financial Implications

Financial implications are central to understanding platforms like Sezzle Pay. The service offers immediate access to goods and services, but this convenience carries specific financial consequences for consumers. Crucially, the structure of installment payments directly affects the total cost of a purchase, often leading to a higher overall price than paying outright. This additional cost arises from interest charges and potential fees, which vary depending on payment plan duration and the specific platform. Real-life examples illustrate this; a consumer purchasing a television might find the total cost over the installment period exceeds the price if paid upfront. This difference should be carefully factored into budget planning.

The importance of understanding these financial implications cannot be overstated. Consumers must critically assess the total cost of the purchase, including interest and fees, over the entire payment period. Comparing this total to alternative financing methods, like using a credit card or personal loan, is essential to make informed financial decisions. Ignoring these implications can lead to unexpected financial burdens, especially if repayment schedules are not adhered to. Missed payments may accrue penalties, further increasing the total cost. Furthermore, the impact on credit scores needs to be evaluated, as failing to meet payment obligations can negatively affect creditworthiness. Consequently, a comprehensive understanding of these details is crucial to maximizing the potential benefits and minimizing the risks of using installment payment platforms. Careful budgeting, clear cost analysis, and realistic repayment projections are necessary for responsible utilization.

In conclusion, the financial implications of using Sezzle Pay, or similar platforms, are multifaceted. The seemingly convenient option of immediate purchase comes with potential additional costs and risks that consumers must diligently assess. Understanding these implications is crucial for responsible financial planning and ensuring a positive experience. Neglecting this aspect could lead to financial difficulties, and recognizing the interconnectedness of installment payments with overall financial health is essential for informed consumer choice.

8. Credit score impact

Platforms like Sezzle Pay, offering installment payment options, can significantly affect credit scores. This impact hinges on responsible use and adherence to payment terms. Understanding how these services influence creditworthiness is crucial for individuals considering using such platforms.

- Reporting to Credit Bureaus

A key aspect is how Sezzle Pay, or similar platforms, report payment activity to credit bureaus. Consistent timely payments positively affect credit scores, demonstrating responsible financial management. Conversely, missed or late payments negatively impact creditworthiness, potentially lowering credit scores. This reporting directly links payment behavior to credit history, a factor scrutinized by lenders when evaluating loan applications.

- Impact of Payment History

Payment history holds substantial weight in determining creditworthiness. Consistent on-time payments create a positive credit history and positively influence credit scores. Conversely, missed or late payments can significantly diminish credit scores, potentially impacting future borrowing opportunities and increasing interest rates. This principle underscores the importance of adhering to payment schedules when using Sezzle Pay or similar services.

- Credit Utilization Rate

The utilization of available credit plays a crucial role in credit scoring. Large balances on revolving credit lines, such as credit cards, reflect high utilization rates. Using Sezzle Pay for larger purchases can indirectly influence credit utilization, potentially affecting credit scores if not carefully managed. A consumer might already have high credit card balances, making Sezzle Pay purchases a factor that could negatively impact credit utilization.

- Potential for Negative Impacts

Using Sezzle Pay, or similar platforms, may create challenges for consumers with existing credit issues or limited credit history. Missed or late payments can quickly lower scores, making it difficult to obtain loans or secure favorable financing in the future. Consumers should recognize that these services are not necessarily free; additional costs, such as interest charges and fees, should be factored into any budgeting or financial planning calculations.

In conclusion, understanding how Sezzle Pay, or similar installment payment platforms, impact credit scores is vital. Responsible utilization, characterized by timely payments and careful budgeting, can contribute to maintaining or improving credit scores. Conversely, a lack of discipline in repayment can negatively affect future financial opportunities. Consumers should evaluate the overall financial implications and how their payment history will align with their current and future financial goals before using such services. Credit scoring is intricately linked to financial responsibility, and consumers must consider the long-term implications of their choices when utilizing installment payment platforms.

Frequently Asked Questions about Sezzle Pay

This section addresses common questions about Sezzle Pay, providing clear and concise answers to help users understand the service's features, benefits, and potential implications.

Question 1: What is Sezzle Pay?

Sezzle Pay is a platform that allows users to make purchases now and pay later in installments. This deferred payment option enables consumers to acquire goods and services without needing to pay the full price upfront. The platform provides flexible payment plans, allowing users to choose their payment schedules and durations.

Question 2: How does Sezzle Pay work?

Users choose Sezzle Pay as a payment option at the point of sale. The platform generates a customized payment plan, outlining the payment schedule and total cost, including potential interest or fees. Users make regular installment payments over a predetermined period, typically months. Failure to meet payment obligations may result in penalties.

Question 3: What are the benefits of using Sezzle Pay?

The primary benefit is immediate access to desired goods or services. Flexible payment terms cater to various financial situations. Retailers often benefit from increased sales volume. However, users should carefully consider the total cost, including potential interest and fees, over the entire payment period.

Question 4: Are there any risks associated with using Sezzle Pay?

Overspending and accumulating debt are potential risks if not managed responsibly. The total cost of the purchase, including interest and fees, may exceed the initial price if paid upfront. Missed or late payments can negatively affect credit scores.

Question 5: How does Sezzle Pay impact credit scores?

Payment history is a critical factor. On-time payments contribute positively to credit scores. Missed or late payments can negatively impact creditworthiness, influencing future borrowing opportunities. Users with existing credit issues or limited credit history should carefully evaluate the potential impact.

Question 6: What are the payment terms and conditions?

Payment terms and conditions vary depending on the specific purchase and the user's agreement with Sezzle Pay. Understanding the total cost, interest rates, fees, payment schedules, and potential penalties is crucial. Review the terms carefully before agreeing to the payment plan.

By understanding the key aspects of Sezzle Pay, users can make informed financial decisions and leverage the service responsibly, ensuring a positive financial experience. Further research into personal financial management strategies is recommended for optimal results.

The next section will delve into the impact of Sezzle Pay on the broader economic landscape.

Sezzle Pay

Sezzle Pay, as a payment platform, offers a unique approach to purchasing. Understanding the potential benefits and risks associated with installment plans is crucial for responsible financial management. These tips aim to provide a framework for evaluating the service and optimizing its use.

Tip 1: Thoroughly Review Terms and Conditions. Carefully scrutinize the complete agreement, including interest rates, fees, and repayment schedules. Do not rely solely on initial marketing materials. A precise understanding of potential penalties for late or missed payments is essential. Analyze the total cost of the purchase over the payment plan's duration, comparing it to alternative financing options.

Tip 2: Assess Affordability. Calculate the monthly payment amount and its impact on existing financial obligations. Consider potential unexpected expenses and whether the installment plan aligns with overall budget constraints. Avoid overextending financial resources to accommodate short-term conveniences.

Tip 3: Monitor Payment Schedules. Establish a system to track and monitor scheduled payments, ensuring timely remittances to avoid penalties. Consider setting up reminders or utilizing payment app notifications to maintain accountability.

Tip 4: Understand the Impact on Credit Scores. Recognize that missed or late payments can negatively affect creditworthiness. This influence on credit scores has substantial implications for future borrowing opportunities. Maintain a history of timely payments to uphold and potentially enhance credit standing.

Tip 5: Compare with Traditional Financing Options. Before committing to Sezzle Pay, compare the overall cost of the purchase under the installment plan with traditional financing methods, like credit cards or loans. Factor in interest rates, fees, and potential penalties to make a well-informed decision.

Tip 6: Avoid Overspending. The perceived ease of acquiring goods immediately using installment plans can potentially lead to overspending. Maintain a focus on realistic budget management and avoid expanding existing financial liabilities beyond manageable levels.

Tip 7: Be Aware of Hidden Fees. Scrutinize the payment plan for additional charges beyond the advertised interest rates. Ensure a thorough understanding of any transaction fees or penalties associated with the platform. Analyze the total cost and thoroughly evaluate all associated charges.

Following these guidelines facilitates informed decision-making and responsible financial management when using Sezzle Pay. Responsible use of such services will likely improve the user experience and minimize the potential for financial difficulties.

These considerations form the basis for informed financial decisions regarding installment payment options. A thorough understanding of the terms, conditions, and potential risks is crucial to safeguarding financial well-being. Further research into consumer financial literacy strategies is strongly advised.

Conclusion

Sezzle Pay represents a significant shift in consumer purchasing behavior. The platform facilitates immediate access to goods and services, but this convenience is accompanied by complex financial implications. Key aspects explored include the nature of installment payments, the impact on credit scores, the relationship between payment durations and interest rates, the role of retail partnerships, and the overall financial consequences for consumers. The potential benefits of broadening access to products and stimulating retail activity must be weighed against the risks of potentially higher total purchase costs and the necessity of responsible financial planning. Consumers should exercise caution in utilizing Sezzle Pay, understanding the implications of interest rates and fees, and diligently tracking payment obligations to maintain financial stability.

Sezzle Pay's success hinges on its ability to balance consumer accessibility with prudent financial management. Careful consideration of terms, thorough cost analysis, and responsible budgeting are paramount for users. This approach minimizes the potential for financial strain and leverages the service's convenience without jeopardizing long-term financial well-being. Future analysis should extend to examining the broader economic impact of such installment payment platforms and their potential influence on consumer behavior and market trends. Understanding the nuances of Sezzle Pay and similar services is critical for both consumers and financial institutions to adapt to the evolving landscape of modern commerce.