A physical location of a financial institution, equipped to process direct deposit transactions, facilitates the transfer of funds from a payer (e.g., employer) to a recipient's account. This can involve the submission of deposit forms, or a specific process for direct deposit initiation. The location may also provide support for troubleshooting direct deposit issues.

These facilities are crucial for individuals who prefer in-person interaction for direct deposit transactions. They offer a tangible point of contact for resolving issues, such as account verification or processing errors. Historically, these branches served as the primary method of initiating and managing direct deposit, although online and mobile banking have become increasingly prevalent. Their continued relevance stems from the enduring value they provide for individuals requiring assistance or preferring direct interaction.

This overview of bank locations specializing in direct deposit procedures sets the stage for exploring the nuances of banking infrastructure and the varying degrees of access to banking services. Further discussion will delve into the advantages of online and mobile platforms compared to in-person transactions, as well as the range of banking support services available.

Bank Branch for Direct Deposit

A bank branch dedicated to direct deposit transactions offers essential services for financial management. Understanding these aspects is crucial for a comprehensive view of this banking function.

- Physical location

- Transaction processing

- Account access

- Support services

- Security measures

- Customer interaction

- Form completion

- Problem resolution

These key aspects of bank branches for direct deposit underscore the essential role they play. A physical location provides a point of contact for direct engagement. Transaction processing and account access are core functions, while support services address customer needs. Security procedures safeguard sensitive financial data. Customer interaction ensures a streamlined process. Form completion, for example, often involves completing paperwork to initiate a direct deposit. Finally, problem resolution addresses potential issues. Efficient resolution of difficulties is critical for maintaining a smooth and reliable process for individuals relying on direct deposit for their income.

1. Physical Location

A physical location, in the context of a bank branch specializing in direct deposit, serves as a tangible point of contact for crucial financial transactions. Its presence offers distinct advantages over purely digital methods. This direct interaction is particularly valuable for those requiring immediate assistance or preferring face-to-face interaction.

- Accessibility and Convenience

A physical branch provides a readily available location. Customers can physically visit to initiate direct deposit arrangements, resolve immediate issues, or confirm details. This convenience is often paramount for individuals unfamiliar with online banking processes or those needing to complete necessary documentation in person. For example, individuals who are new to a region or those who are less digitally fluent may find navigating bank services in person more accessible.

- Security and Trust

Direct interaction with a physical location fosters a sense of security and trust. Customers can observe the environment, interact with staff directly, and have their questions answered in a controlled, secure setting. This personal interaction is particularly important when dealing with sensitive financial transactions. For example, the presence of security measures, staff members, and secure facilities enhances the confidence of customers seeking this form of support.

- Personal Assistance and Support

Bank branches provide personalized support. Staff can assist customers in completing forms, address issues related to the direct deposit process, and clarify any doubts or concerns. This hands-on support is particularly relevant for complex transactions or those who need detailed explanations. This personalized approach ensures accurate setup and problem resolution.

- Account Verification and Proof of Identity

A physical location facilitates secure account verification and proof of identity. Physical presence verifies the individual's identity and authenticity, an essential component of safeguarding accounts. The bank employs methods like verifying identification documents, enabling accurate account handling. This process ensures that only authorized individuals access direct deposit services.

In summary, the physical presence of a bank branch for direct deposit is more than just a location; it's a critical component of the financial service ecosystem. The benefits of accessibility, security, support, and identity verification contribute significantly to a positive customer experience and the smooth operation of direct deposit transactions. These factors, while not exclusive to in-person interactions, are particularly significant in the context of direct deposit transactions.

2. Transaction processing

Transaction processing forms the bedrock of a bank branch dedicated to direct deposit. Efficient processing of direct deposit transactions is paramount. This function involves receiving instructions, validating data, initiating transfers, and recording details. A bank branch's role in direct deposit is intrinsically linked to the accurate and timely execution of these procedures. Inaccurate or delayed processing can lead to significant financial disruptions for both the payer and recipient.

Consider a scenario where an employer initiates a payroll direct deposit. The bank branch must accurately receive the transaction details, validate the recipient's account information, and initiate the transfer. Any error, such as an incorrect account number or insufficient funds, requires immediate resolution to avoid payment delays and potential disputes. Inaccurate or untimely processing can result in financial hardship for employees relying on their salaries and disrupt business operations. The smooth execution of these procedures relies heavily on the efficiency and accuracy of the bank branch personnel and the bank's internal systems.

Understanding the intricate connection between transaction processing and a bank branch for direct deposit reveals the critical role of these locations. Accurate and timely processing is essential for the reliability of the financial system and for maintaining the trust of individuals and institutions who rely on this service. Failures in this process can result in significant financial ramifications. Thus, robust internal controls, skilled personnel, and secure systems are vital components of successful transaction processing within such a branch. This understanding is critical for anyone involved in the financial industry or dealing with direct deposit services.

3. Account access

Account access is intrinsically linked to the function of a bank branch dedicated to direct deposit. The branch's role isn't merely processing transactions; it facilitates access to accounts. This access is crucial for verifying account details, resolving discrepancies, and, in some cases, for initiating direct deposit arrangements. Accurate account access procedures are essential for the security and reliability of the direct deposit process.

Consider a scenario where an employee's direct deposit is delayed. A bank branch can facilitate account access to verify the account number's accuracy. By confirming the recipient's account details, the branch can identify and resolve any potential errors. This access enables swift reconciliation of the transaction. Similarly, if a customer needs to modify their direct deposit details, account access empowers them to initiate such changes safely and reliably through the branch. Proper account access is essential for both preventive and remedial actions. Without appropriate access, direct deposit transactions become vulnerable to errors and disputes.

The practical significance of understanding this connection between account access and bank branches lies in its impact on the efficiency and security of the entire financial process. Thorough account access procedures contribute to the reliability of direct deposit. Without seamless account verification and modification capabilities, direct deposit services suffer significant credibility issues. This understanding is critical for institutions to ensure smooth operations, maintain customer trust, and prevent fraudulent activity. A robust system of account access procedures within a bank branch enhances the reliability of direct deposit and minimizes potential disruptions to financial transactions.

4. Support services

Support services are an integral component of a bank branch specializing in direct deposit. These services address the diverse needs of customers interacting with the branch for direct deposit transactions. Effective support mitigates potential issues and ensures a seamless experience for clients. Without robust support, even well-designed direct deposit systems can falter, leading to delays, errors, and customer dissatisfaction. For example, a customer experiencing technical difficulties initiating a direct deposit transfer requires prompt and knowledgeable support to resolve the problem promptly.

Support services encompass a range of activities, from resolving account access issues to guiding customers through the direct deposit setup process. Comprehensive support procedures address various scenarios. For instance, an employee who has recently changed banks or accounts may require assistance in updating their direct deposit information. A clear and concise onboarding process for direct deposit, available at the branch, reduces confusion and increases user satisfaction. Moreover, assistance in troubleshooting technical issues, resolving discrepancies, or rectifying errors are all crucial support services that ensure the stability and reliability of direct deposit systems. This detailed guidance for customers reduces frustration and promotes a positive experience.

The practical significance of understanding the link between support services and bank branches for direct deposit lies in the crucial role support plays in maintaining the integrity and efficiency of the financial system. Customers who encounter issues with their direct deposit often rely heavily on the branch's support resources to resolve problems. The provision of prompt and efficient support reflects positively on the institution and fosters trust among clients. A well-structured support infrastructure ensures accuracy and timeliness in direct deposit transactions, minimizing the risk of financial errors and maintaining the reliability of the system. Failing to provide adequate support can lead to decreased customer loyalty, increased administrative burden, and potential reputational damage.

5. Security measures

Security measures are inextricably linked to the operation of a bank branch focused on direct deposit. These measures safeguard sensitive financial data, protect against fraud, and ensure the integrity of transactions. Robust security protocols are essential to maintain public trust and prevent financial losses. Compromised security can result in significant reputational damage and financial penalties for the institution.

Implementing comprehensive security measures at a bank branch for direct deposit necessitates a multi-faceted approach. This includes physical security, such as secure facilities and controlled access; technological security, encompassing encryption and secure network systems; and procedural security, encompassing rigorous verification procedures and staff training. For example, strict authentication protocols verify the identity of individuals initiating direct deposit changes. Security cameras and personnel monitoring help deter unauthorized access and activities. Secure handling of sensitive documents minimizes the risk of data breaches. The consistent application of these security protocols minimizes the risk of errors and fraudulent activities. Failure to implement adequate measures can lead to severe consequences, like compromised account security and financial losses.

Understanding the critical connection between security measures and bank branches for direct deposit is vital. Robust security protocols build trust and confidence among customers. This fosters reliability in financial transactions and safeguards against fraud. Without these measures, the entire financial system, and the individual customers reliant on it, becomes vulnerable to significant financial harm. The ongoing development and adaptation of security measures to emerging threats are essential for protecting the integrity of direct deposit systems and maintaining public trust. A comprehensive approach to security empowers institutions to effectively protect sensitive data and maintain confidence in their services.

6. Customer interaction

Effective customer interaction is a cornerstone of any successful bank branch specializing in direct deposit. The nature of this interaction varies, from in-person consultations to phone support, and profoundly influences the overall success of the direct deposit process. Direct engagement allows for immediate issue resolution, personalized guidance, and the cultivation of trust, factors critical for a smooth customer experience. A branch's ability to handle complex inquiries and provide support demonstrates a commitment to reliability and facilitates a secure environment for financial transactions. For example, a customer experiencing difficulties with a direct deposit from a new employer can receive personalized guidance on completing necessary forms directly within the branch. This ensures a positive outcome and reduces the customer's stress level during a potentially complex financial process. This personal touch builds loyalty and fosters long-term relationships with customers.

The importance of customer interaction in this context extends beyond problem-solving. It encompasses the initial setup of direct deposit, offering clarity on procedures, and proactively addressing potential difficulties. A well-informed customer is less likely to encounter problems and more inclined to maintain positive relationships with the institution. For instance, during the initial direct deposit setup, clear explanations of the process, the advantages of using a bank's direct deposit system, and the safety features of the institution are valuable. Such proactive communication fosters customer confidence and strengthens the bank's reputation. Further, well-trained staff capable of navigating complex customer inquiries and adept at providing clear, simple explanations is crucial. This kind of interaction minimizes confusion and streamlines the process, particularly for those less familiar with financial technologies.

In conclusion, effective customer interaction is not merely an aspect of a bank branch for direct deposit; it is a cornerstone. Strong customer relationships are critical in establishing trust, encouraging repeat business, and mitigating the potential for problems. The branch's ability to provide timely, comprehensive, and personalized support directly impacts the user experience and the overall success of direct deposit transactions. The practical implications of this understanding extend beyond individual transactions, influencing broader aspects of financial institution reputation, customer loyalty, and the efficient operation of the banking system as a whole. Robust customer interaction strategies can translate to tangible improvements in various facets of a financial institution's operations. This includes reduced error rates, enhanced customer satisfaction, and ultimately, a more reliable financial system.

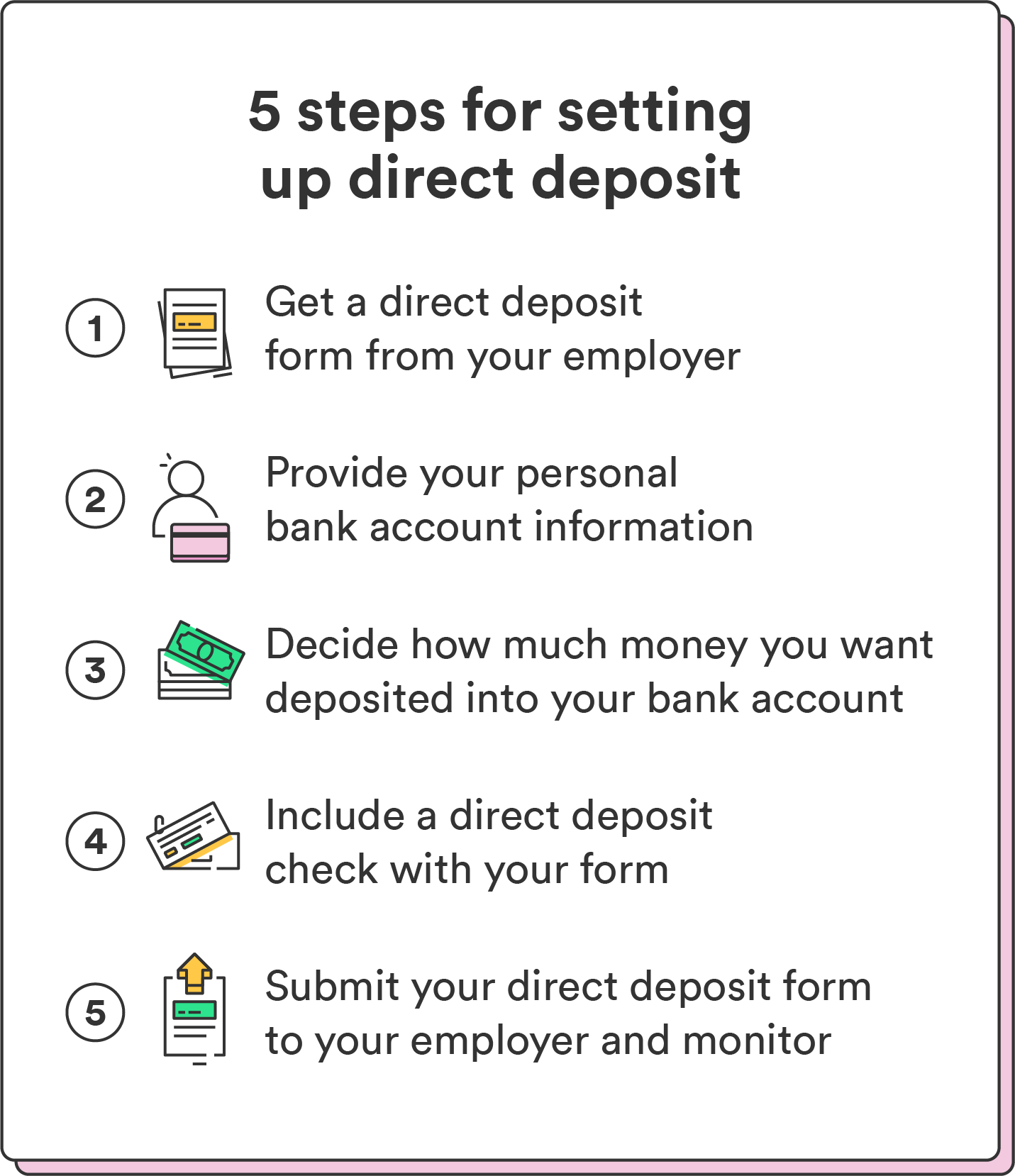

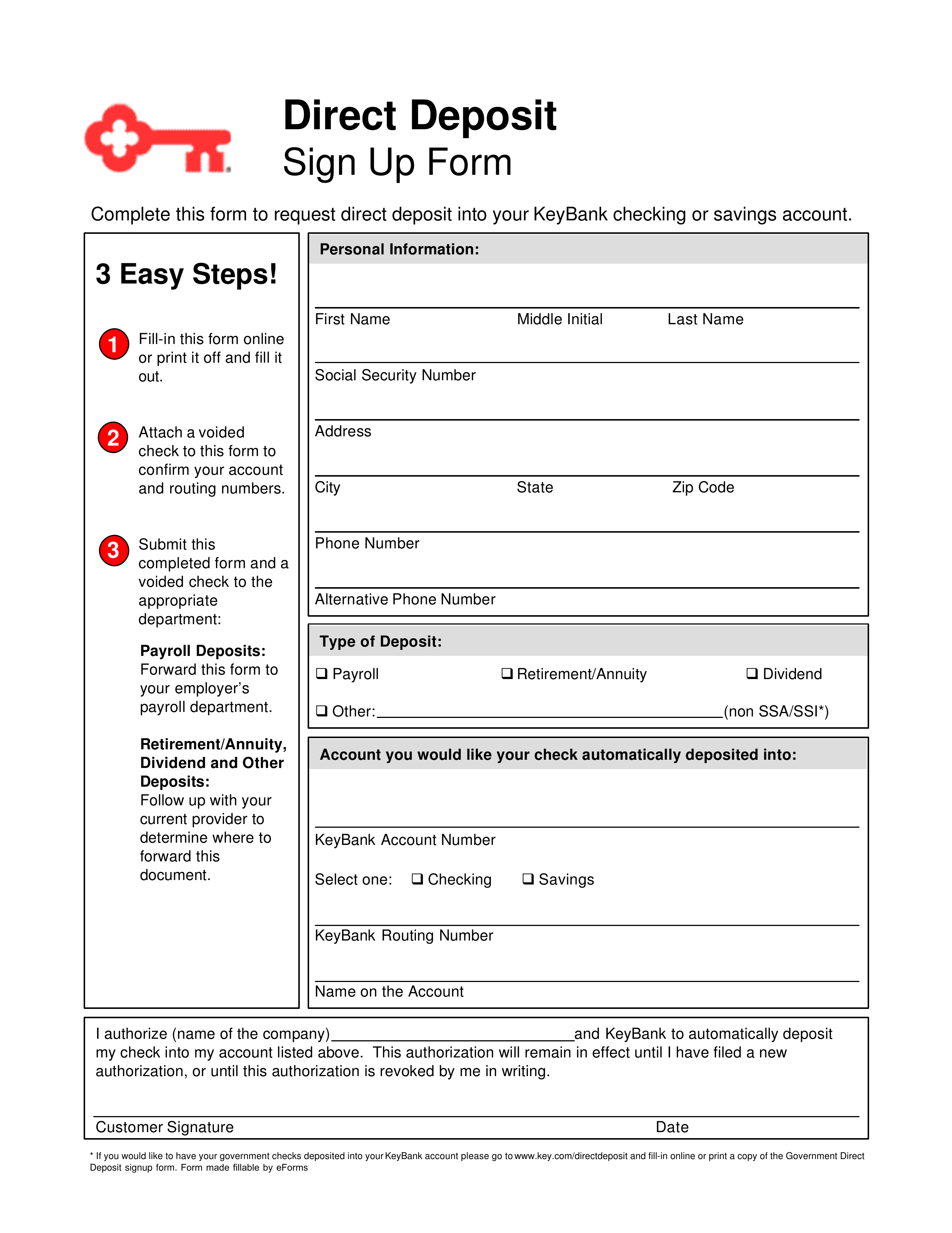

7. Form completion

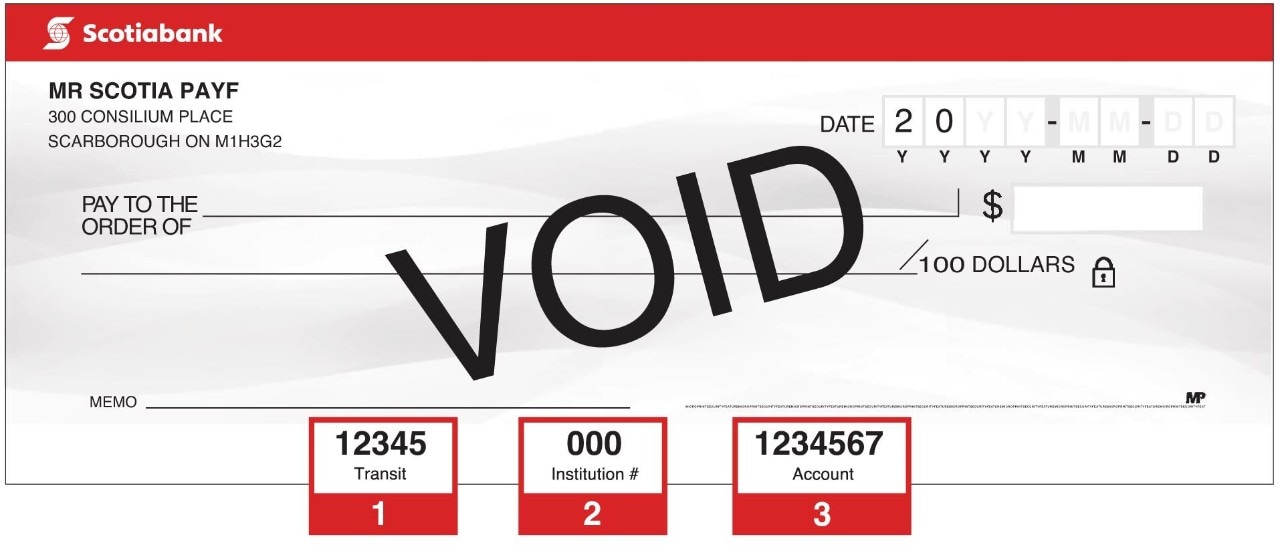

Accurate and timely form completion is a critical component of direct deposit transactions within a bank branch. Form completion initiates the process, ensuring correct data entry and facilitates the transfer of funds. Incorrect or incomplete forms lead to delays, errors, or even rejection of transactions. This process is essential for the security and accuracy of the entire financial exchange. For instance, an employee completing a direct deposit form must accurately provide their bank account details. If the information is incorrect, the deposit will not reach the intended account.

The importance of form completion extends beyond the immediate transaction. Properly completed forms establish a verifiable record of the transaction, aiding in dispute resolution if issues arise. Accurate information ensures the correct amount is deposited into the correct account. Incomplete forms potentially expose the system to fraud. For example, if a form lacks crucial verification details, the risk of unauthorized access to funds increases. Thus, the integrity of the direct deposit process hinges significantly on the precision and completeness of these forms.

Understanding the connection between form completion and bank branch operations highlights the importance of standardized procedures. Standardized forms, clear instructions, and readily available support during form completion are crucial. A lack of clear guidance can lead to errors and increase administrative burdens. For example, a bank branch equipped with user-friendly forms and readily available assistance during the form completion process facilitates a streamlined operation, reducing the risk of errors and enhancing customer satisfaction. This understanding underscores the need for a robust system for form creation, management, and validation within the bank branch. Comprehensive training programs for staff handling these forms ensure accuracy and efficiency, contributing to a secure and reliable direct deposit system.

8. Problem resolution

Effective problem resolution within a bank branch dedicated to direct deposit transactions is crucial for maintaining customer trust and the integrity of the financial system. Delays or inaccuracies in direct deposit can cause significant hardship for individuals and disrupt the smooth flow of financial activity. Consequently, a streamlined approach to addressing issues promptly and efficiently is essential for a positive customer experience and the bank's reputation.

- Account Verification and Reconciliation

A bank branch plays a critical role in verifying account information and reconciling discrepancies that might arise during a direct deposit transaction. This facet involves confirming account numbers, verifying customer identities, and identifying potential errors in the transfer process. For example, if a direct deposit is rejected due to an incorrect account number, the branch staff must accurately identify the error and guide the customer to correct the information. This process directly impacts the accuracy and timeliness of the transaction and safeguards the customer's funds.

- Technical Issues Resolution

Technical glitches in the system can lead to direct deposit failures. Resolution of such problems requires a bank branch to diagnose and resolve technical issues that hinder the transfer process. This encompasses identifying system errors, ensuring data integrity, and restoring functionality. For example, if a network outage affects the bank's online systems, the branch can offer in-person support and processing of direct deposits through manual methods until the issue is resolved. This demonstrates the adaptability of the branch to maintain continuity of service.

- Dispute Resolution and Customer Support

A bank branch acts as a crucial point of contact for customers facing disputes related to direct deposit transactions. This facet involves effectively resolving customer complaints and disputes regarding incorrect amounts, missing payments, or delayed transfers. Clear communication, documentation, and adherence to established procedures are key elements in handling these situations. For example, a customer who believes they haven't received a full salary deposit can report the issue to the branch, allowing the staff to investigate the claim, verify details, and ensure a satisfactory resolution.

- Policy Adherence and Compliance

Maintaining adherence to internal policies and relevant regulatory guidelines is crucial for effective problem resolution. Branch staff must understand and adhere to established protocols to prevent errors and ensure compliance. For example, if a customer requests a direct deposit change without proper documentation, staff must follow the bank's policy to verify their identity before processing the request. This facet ensures the branch operates within legal boundaries and safeguards against potential risk.

These facets highlight the intricate connection between problem resolution and a bank branch focused on direct deposit. A strong problem resolution framework ensures the smooth execution of direct deposit transactions, safeguards customer funds, upholds the bank's reputation, and reinforces trust in the financial system. A bank's ability to resolve issues quickly and effectively is critical in the modern financial landscape where customers increasingly rely on the timely processing of direct deposits.

Frequently Asked Questions about Bank Branches for Direct Deposit

This section addresses common inquiries regarding bank branches specializing in direct deposit transactions. Clear answers provide crucial information for navigating this financial service.

Question 1: What are the benefits of using a bank branch for direct deposit?

Bank branches offer in-person assistance, which can be beneficial for individuals needing immediate help with account issues, form completion, or resolving discrepancies. Personal interaction is valuable for those unfamiliar with online banking systems or who prefer face-to-face support. This approach ensures a more personalized and potentially faster resolution of specific problems.

Question 2: Are bank branches for direct deposit still relevant in the digital age?

While online and mobile banking have become increasingly prevalent, bank branches dedicated to direct deposit transactions remain relevant. They provide a vital point of contact for those requiring personalized support, especially when dealing with complex or unusual situations. A physical presence ensures access to assistance for individuals who prefer or require in-person interaction.

Question 3: How can I find a bank branch specializing in direct deposit?

Consult the bank's website or contact customer service. Branch locations may be listed on online directories or through the bank's customer service. Specific inquiry regarding a branch's direct deposit capabilities should be made prior to visiting. Accurate information about a bank's direct deposit capabilities is crucial for a successful visit.

Question 4: What forms or documentation might I need to use a bank branch for direct deposit?

Requirements vary by bank, but often include identification documents, such as a driver's license or passport, and forms specific to the direct deposit transaction, such as payroll information, account verification, or authorization. Contact the bank beforehand to clarify necessary forms and documents.

Question 5: Are there security concerns related to using a physical bank branch for direct deposit?

While physical branches offer a certain level of security, it's vital to be mindful of your surroundings and to only handle sensitive financial documents in secure areas. Bank branches generally employ security measures to protect customer transactions. Maintaining awareness of security procedures and ensuring safety is crucial. Inquire about the branch's specific security policies if there are concerns.

Question 6: What are the typical hours of operation for a bank branch that handles direct deposits?

Bank branch hours for direct deposit services vary. Consult the bank's operating hours and schedule, as these may differ from standard business hours. Direct deposit-specific services may have distinct hours or availability.

A comprehensive understanding of bank branches for direct deposit is crucial, encompassing their continued relevance despite technological advancements and the specific procedures associated with their services. This awareness facilitates a streamlined and secure financial transaction experience. This section provides essential information for navigating the financial services sector and optimizing direct deposit strategies. Further, this overview will be instrumental in a broader examination of financial services access and preferences.

Next, we will explore the comparison between in-person and online methods for direct deposit, highlighting their relative benefits and drawbacks.

Tips for Using Bank Branches for Direct Deposit

Effective utilization of bank branches for direct deposit transactions requires careful planning and awareness of the associated procedures. These tips provide guidance on maximizing the benefits of in-person interactions while maintaining security and accuracy.

Tip 1: Confirm Branch Capabilities. Prior to visiting, verify the branch's specific direct deposit services. Not all branches handle every type of direct deposit transaction equally. Some may specialize in particular types of deposits, such as payroll or government benefits. Ensure the chosen branch can fulfill the intended transaction before arrival. Confirm if the branch supports specific forms, documents, or procedures.

Tip 2: Plan the Visit. Schedule a visit during the branch's operating hours dedicated to direct deposit transactions. This often differs from general operating hours. Clarify anticipated wait times or potential transaction limits. Bringing necessary documentation and forms in advance reduces potential delays. This proactive approach optimizes the visit for efficiency.

Tip 3: Understand Required Documentation. Thoroughly review the necessary documentation and forms required for the specific direct deposit transaction. Ensure all requested information is complete and accurate. Providing accurate details from the outset minimizes potential errors and delays in the transaction processing. Double-checking information minimizes errors and ensures a smooth transaction.

Tip 4: Communicate Clearly with Staff. Engage with staff to clarify any uncertainties regarding the direct deposit process. Ask questions about procedures, timelines, or potential complications to ensure a smooth transaction. Clear communication minimizes misunderstandings and clarifies expectations. This proactive approach to communication ensures a productive interaction.

Tip 5: Maintain Security Awareness. Handle sensitive documents securely and follow branch security protocols. Be mindful of the surrounding environment and avoid revealing sensitive information publicly. Protecting personal information safeguards financial transactions and the security of the institution. Maintaining a vigilant approach to personal safety is essential when interacting with sensitive financial information.

Tip 6: Review Post-Transaction Records. Thoroughly review documentation and confirmation records from the bank branch to confirm the details of the direct deposit. Compare the records with expected amounts, ensuring complete accuracy of the deposit. This ensures the accuracy of transactions and enables prompt identification of potential discrepancies.

Adhering to these tips facilitates smooth and secure direct deposit transactions through bank branches, enhancing the overall reliability and efficiency of the financial process. These practices are crucial in mitigating potential issues, ensuring security, and maintaining a productive interaction with the institution.

By implementing these proactive measures, individuals can optimize their interactions with bank branches, promoting a streamlined and trustworthy direct deposit experience.

Conclusion

The exploration of bank branches dedicated to direct deposit transactions reveals a multifaceted operation crucial to the financial landscape. Key elements, including physical location, transaction processing, account access, support services, security measures, customer interaction, form completion, and problem resolution, highlight the integral role these facilities play. The presence of a physical branch offers tangible benefits, particularly for those requiring in-person assistance or preferring direct engagement. Effective transaction processing, meticulous account verification, and robust support systems contribute to the reliable and secure transfer of funds. Security protocols and adherence to established procedures safeguard sensitive financial data. The interaction between staff and customers plays a pivotal role in addressing issues and building trust. Accurate form completion ensures the integrity of transactions, and efficient problem resolution maintains customer satisfaction. The continued importance of these bank branches, despite the rise of digital platforms, underscores the enduring need for accessible and reliable financial services, particularly for those who require in-person support. Further, the analysis reveals the critical role these branches play in facilitating smooth and secure financial transactions.

The conclusion underscores the enduring significance of bank branches specializing in direct deposit. Their importance in the financial ecosystem cannot be overstated. As financial technology continues to evolve, the ability to offer both digital and physical access to financial services remains essential. The continued presence of robust bank branches dedicated to direct deposit facilitates a vital link between traditional financial practices and the expanding digital sphere. This approach provides a crucial alternative for those who require in-person interaction and assistance in handling sensitive financial transactions. Maintaining a balance between digital convenience and accessible in-person service is critical in ensuring everyone can securely manage their finances.